{kind=link}

Singapore’s lending landscape offers a variety of financing options for businesses, giving entrepreneurs and companies access to capital that can support both short-term needs and long-term ambitions. However, obtaining financing requires more than submitting an application and waiting for approval.

Lenders carefully assess each applicant to understand the level of risk involved and determine whether the business can comfortably meet its repayment obligations. Understanding these evaluation criteria can help you prepare stronger applications and improve your chances of securing a suitable business loan.

Before submitting an application for a business loan in Singapore, consider these key factors that lenders commonly review and recognise how each one contributes to the overall assessment process.

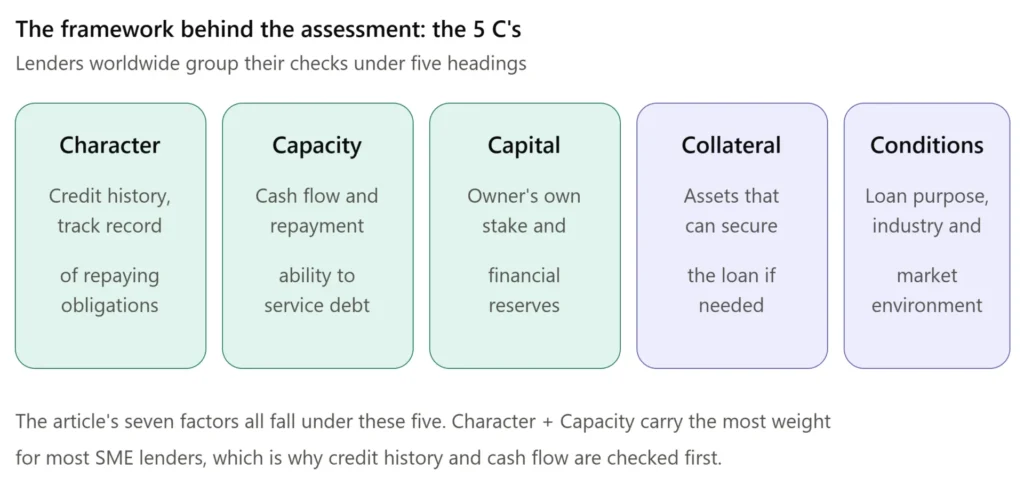

Credit History

Financial habits leave a lasting impression long before a lender reviews revenue figures or business plans. For this reason, one of the first areas lenders examine is credit history, as it provides insight into how responsibly a business and its leaders have managed previous financial obligations. In many cases, lenders may review both the company’s credit profile and the personal credit records of directors or major shareholders, particularly for small and medium-sized enterprises.

A business with a positive credit profile typically inspires greater confidence because it demonstrates an established commitment to meeting financial obligations consistently through timely repayments, prudent borrowing, and responsible financial management. Conversely, missed payments, defaults, or a history of excessive debt can raise concerns about future repayment behaviour.

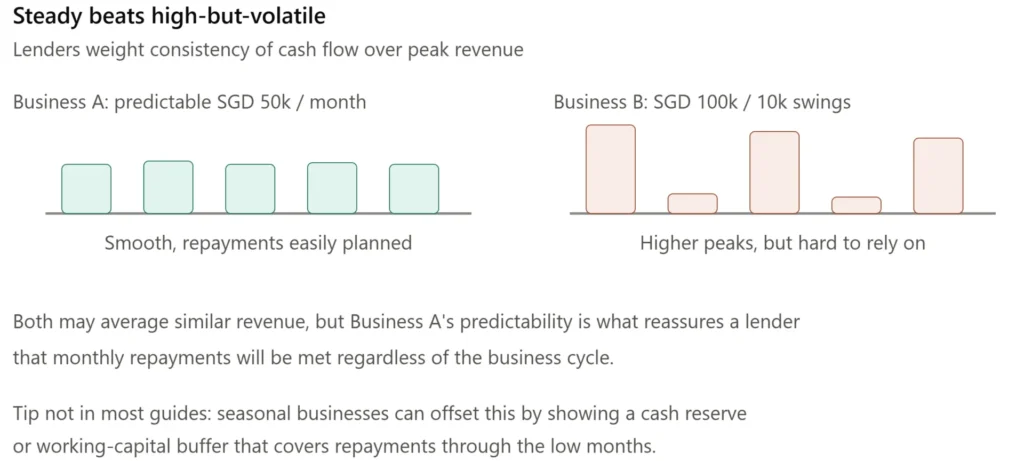

Cash Flow Stability

Lenders typically review bank statements, financial records and transaction histories to assess the reliability of cash inflows. That’s because revenue figures may capture attention, but lenders are more interested in the consistency of incoming cash. A company generating SGD 50,000 monthly with predictable income may appear less risky than one generating SGD 100,000 one month and SGD 10,000 the next.

This is particularly relevant for SMEs with seasonal revenue patterns. Lenders want evidence that cash inflows are sufficiently stable to support regular repayments, regardless of market fluctuations. Companies that experience periodic fluctuations may benefit from showing how they manage working capital and maintain financial stability throughout different business cycles.

Business Performance

Past performance does not guarantee future success, but it can provide valuable insight into a company’s operational health and growth potential. As a result, lenders closely examine financial performance to understand how a business has been performing over time. This includes revenue growth, profitability, customer retention, and overall financial trends. Consistent performance suggests a business has developed sustainable operations and can adapt to changing market conditions.

Lenders also look beyond headline figures to understand the underlying drivers of business performance. A company that demonstrates increasing sales alongside healthy margins may present a stronger case than one that relies on aggressive pricing strategies that limit profitability.

In some cases, lenders may consider industry conditions. Businesses operating in resilient sectors with stable demand may be viewed differently from those facing significant market uncertainty. Presenting financial results within the context of industry performance can help provide a more complete picture of the company’s position.

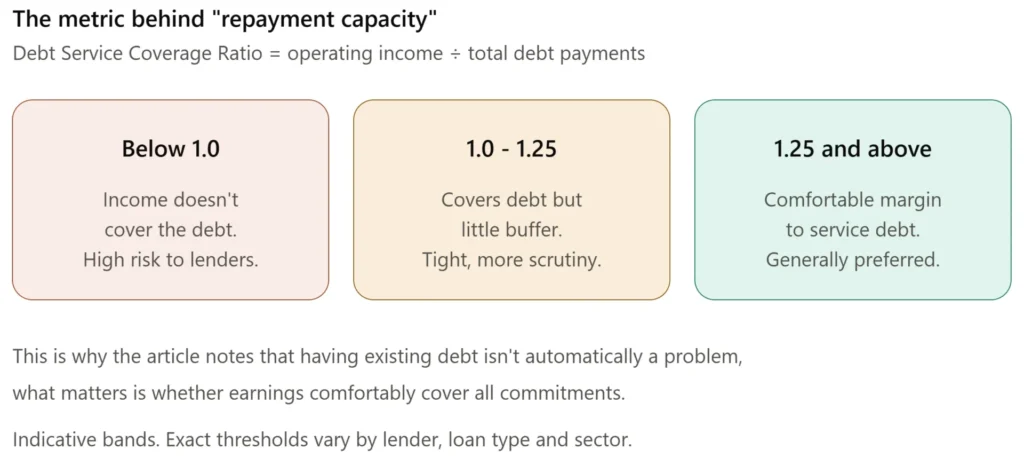

Repayment Capacity

Every lending decision ultimately comes back to one fundamental question: can the borrower comfortably repay the loan? Lenders assess whether a business generates sufficient cash to cover current obligations while taking on additional debt. This analysis includes reviewing existing loans, lease commitments, supplier obligations, and other recurring expenses.

Notably, having outstanding debt does not automatically weaken an application. What matters is whether the business can continue servicing all commitments without placing excessive strain on cash reserves. For example, a growing company may already have financing facilities in place but still demonstrate strong repayment capacity due to healthy earnings and positive cash flow. On the other hand, a business with limited financial flexibility may face greater scrutiny even if its overall debt level appears modest.

Business Model and Revenue Sustainability

Numbers tell part of the story, but lenders also want to understand how a business generates those numbers in the first place. Evaluating the business model helps them assess whether current performance is likely to continue in the future. Businesses that rely heavily on a single customer or a small group of clients may face additional scrutiny because the loss of a key account could have a substantial impact on future revenue.

Similarly, lenders may consider whether the company’s products or services remain relevant within the current market environment. A business operating in a growing sector with clear demand drivers may inspire greater confidence than one facing significant competitive or structural challenges.

Loan Purpose

A well-reasoned explanation for the funding requirement can strengthen the overall credibility of the application. Lenders generally prefer to see a clear, practical reason for borrowing that aligns with the company’s operational needs or growth plans. This could be purchasing equipment, financing inventory, expanding into new markets, hiring additional staff, or strengthening working capital to support business growth.

A clearly defined purpose also allows lenders to evaluate how the financing may contribute to future business performance. It demonstrates that management has carefully considered how the borrowed funds will be utilised and how the investment supports broader business objectives.

Documentation and Financial Transparency

Lenders rely on financial statements, bank records, tax documents, business profiles and other supporting materials to validate the information presented in an application. For this reason, well-organised documentation reflects good financial management and allows lenders to conduct their assessment more efficiently.

Transparency is equally important. Businesses that provide clear explanations for financial trends, unusual transactions, or existing liabilities often create greater confidence during the review process. In contrast, missing information or inconsistencies may lead to additional questions and delays.

Maintaining accurate financial records throughout the year can therefore provide benefits that extend far beyond compliance requirements. It also helps position the business favourably when financing opportunities arise.

Get Approved for a Business Loan in Singapore

Ultimately, a successful loan application is the result of preparation rather than timing. Businesses that maintain strong financial discipline, demonstrate transparency, and understand how lenders assess risk are typically better positioned when seeking financing.